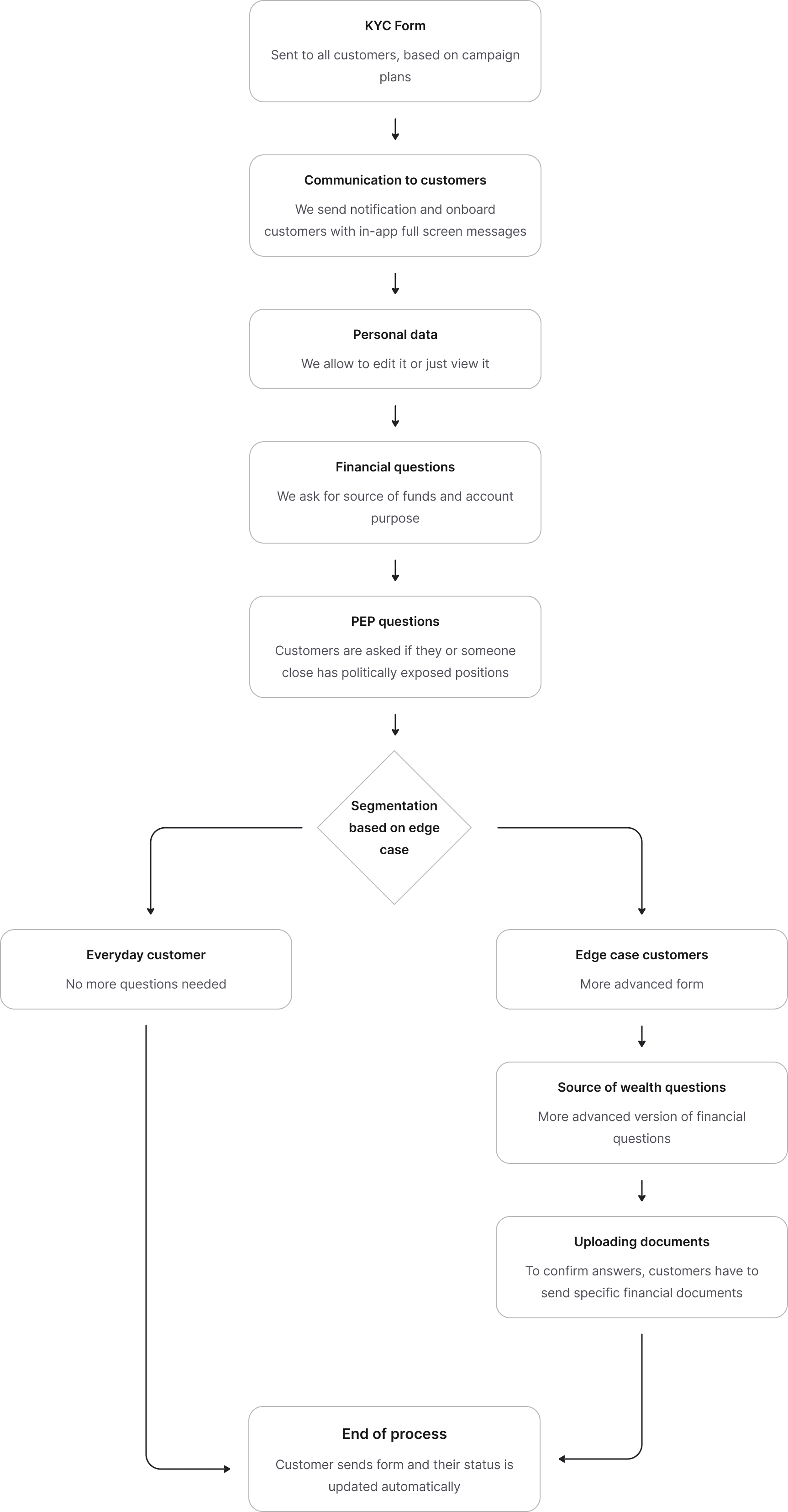

Banks are legally required to keep up-to-date information about their customers' financial situation. This is handled through KYC (Know Your Customer) verification: confirming identity, financial profile, and a few regulatory data points. In essence, it can be a survey for the customer to fill in.

Customers have very different expectations. For them, this can feel like a violation of their privacy. A bank asking sensitive financial questions comes as a surprise, and the natural reaction is suspicion.

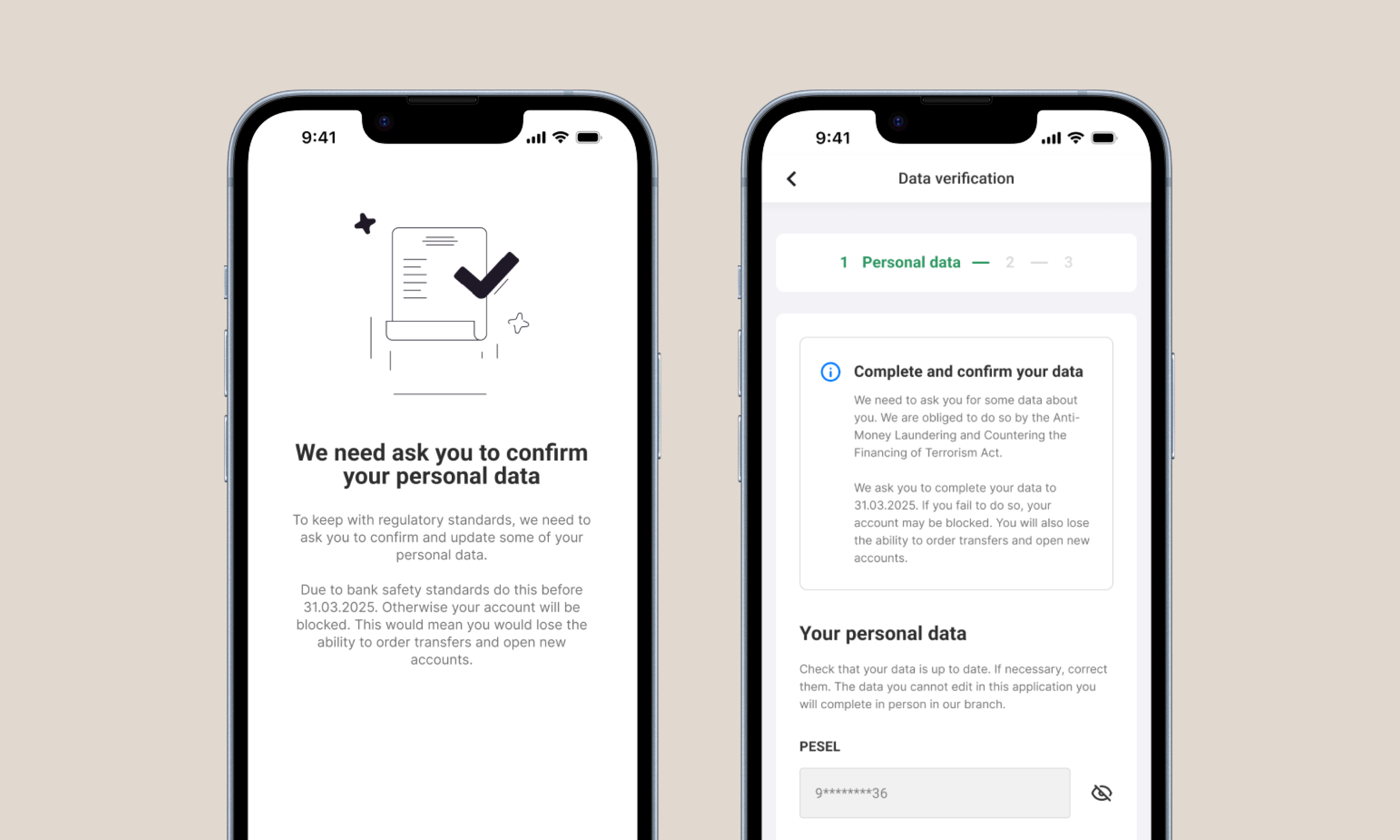

There are consequences on both sides. A customer who ignores KYC risks having their account restricted. The bank faces regulatory exposure, and failing to gather this data can lead to real legal consequences.

What's the scope, then?

This project isn't just about designing a survey. It's about creating an experience built on trust and understanding while covering regulatory needs. There were several issues to tackle at once:

- Project within highly regulated industry. Several pieces of information we had to gather were unchangeable. It was about reframing them, not designing an alternative.

- It is for whole customer base. Use cases ranged from the most common to the most unusual: driven by a customer's products, nationality, or even geographical location.

- It is a multi-channel experience. This project goes beyond app process. It lives alongside its own communication layer: notifications, in-app messages and direct contact with bank call center team.

This project focuses on the digital experience. There was also an analog version, conducted in bank branches, since not every customer has access to digital channels.

What's the goal?

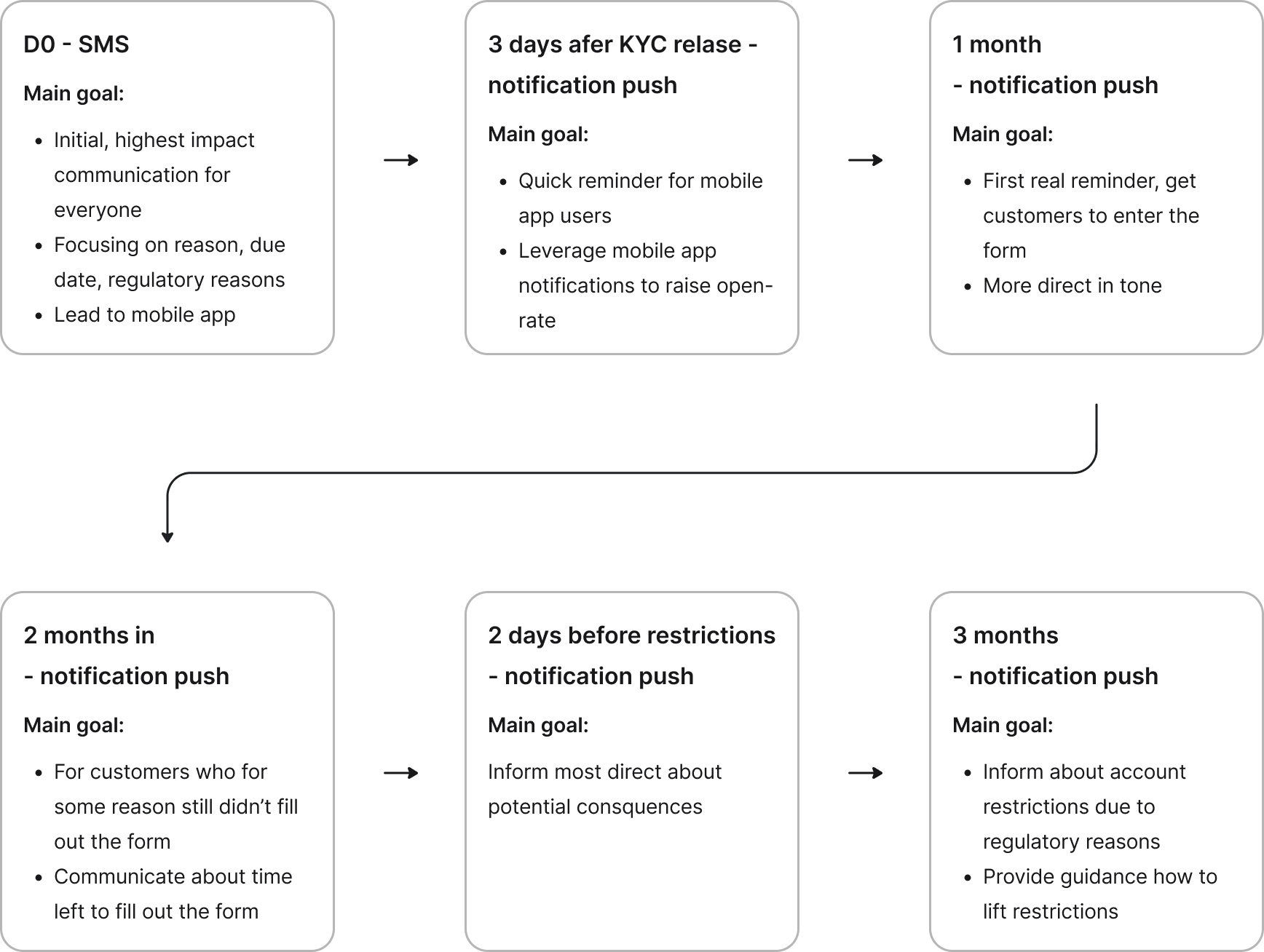

The regulatory background meant the form was mandatory. On the timeline, customers had 3 months to fill it in from the moment they received it. After that it was still possible to complete, but we wanted to avoid that because of the possible consequences for the customer, such as having the account restricted.

Because of that, as close to 100% completion rate as possible was defined as main metric to follow.